“In Insurance, Location is Everything” is our second in a series of blog posts exploring how various industries are taking advantage of big data and analytics. To read more, download our entire eBook, “How Big Data is Changing Industries.”

“In insurance, location is everything. It helps insurers understand where the risks are, whether there has been accidental (or deliberate) accumulation of risk and where their customers are.” – Tony Boobier, Analytics Leader – Insurance, IBM

Big Data, Big Business

Most aspects of our personal lives relate to location. Many businesses realize that and are now using systems to capture, store, analyze, and visualize location data to gain valuable customer insights.

These data help them geo-target sales, manage supply chains, and evaluate risk, providing businesses with new possibilities.

Insurance Relies on Location

Likewise, in insurance, nearly every data point has some relationship to location. First of all, location data helps insurance companies advertise their services, find their customers and analyze potential risks. Also, an insurer’s distribution strategy, claims services deployment, and supply chain management systems run smoothly by utilizing location data.

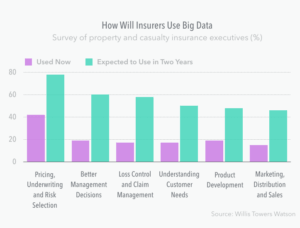

Location Data for Better Risk Modeling, Underwriting, and Pricing

Most noteworthy, P&C insurers can immediately benefit vast location data to better model risk and dramatically improve their underwriting and pricing. Some examples of this location data include:

- Crime Risk Data. Crime risk data and theft and vandalism frequency data, including past, present, and projected crime risk scores, give insurers underwriting and pricing advantages.

- Fire Risk Data. For most carriers, fire represents a huge loss. Accurate data on fire risk and predictive modeling can help insurers minimize losses and improve performance.

- Foreclosure Alerts. A property in foreclosure carries a much higher risk of vandalism, arson, or other damage. Actionable data on properties currently or previously in foreclosure allows insurers to assess risk exposure and act accordingly.

- Catastrophe Risk Data. Using modern analytics, insurers can better manage catastrophe risk. This data can be used for accurate risk assessments based on a customer’s location.

- Behavioral Data. Human behavior is usually not well represented in insurers’ risk models. Behavioral models allow insurers to price policies for risks associated with behavior-related losses, such as fire, crime, auto, liability, water damage, and even wind and hail damage.

- Property Data. Residential property characteristics data and predictive analytics help insurers assign price to risk more accurately.

- Latitude/Longitude. Data on latitude/longitude-based risk areas provide companies with a competitive edge by letting them incorporate a more appropriate picture of homeowners’ risks into rating and underwriting decisions.

In conclusion, for many, location data still equates to just mapping and statistics. However, with recent technology developments, such as connected car, connected home, and predictive analytics, as well as the ability to record, store, and analyze data, the competitive landscape is sure to change.